What Is an HMO Rental Yield Calculator?

An HMO Rental Yield Calculator helps property investors estimate the financial performance of a house in multiple occupation before committing capital to a purchase.

HMO investments can generate higher rental income than single-let properties, but they also involve more complex costs, regulation, operating assumptions, and regional tax treatment.

This calculator helps investors understand:

Gross rental income

Occupancy-adjusted income

Monthly operating costs

Net monthly income

Gross yield

Net yield

Regional property purchase tax

One-off purchase costs

Refurbishment costs

Total capital required

Rather than relying on a simple rent-versus-property-price calculation, the model uses individual room rents, expected occupancy, operating costs, ownership type, purchase region, and acquisition costs to estimate investment performance.

Large HMOs may require a licence where 5 or more people from more than one household share facilities, and smaller HMOs may also require licensing depending on local council rules.

How This HMO Rental Yield Model Works

The calculator estimates HMO investment performance by modelling both income and cost.

It starts with the property purchase price, location, ownership structure, and number of rentable units. It then builds up expected rental income from each room or unit and adjusts this by an assumed occupancy rate.

The model also includes operating costs, property management fees, leasehold charges, refurbishment costs, and one-off purchase fees.

Purchase Region

The calculator allows the investor to select whether the property is in England, Scotland, or Wales.

This matters because property transaction taxes differ by region.

England uses Stamp Duty Land Tax, Wales uses Land Transaction Tax, and Scotland uses Land and Buildings Transaction Tax. Higher rates can apply to additional residential properties.

Property Purchase Price

The capital value is the price paid for the property.

This is one of the most important drivers of yield because it determines both the size of the investment and the likely property transaction tax due.

Number of Rentable Units

The model allows the investor to define the number of rentable rooms or units.

Each unit can have its own monthly rent assumption, making the model more accurate than using a single blended rent figure.

Room-Level Rental Values

The calculator models expected rent for each unit individually.

This is useful for HMOs because room values can vary depending on size, ensuite access, kitchenette access, furnishing level, and perceived tenant value.

Refurbishment Costs

The model includes optional capital expenditure for refurbishment or renovation work.

This helps investors understand the true capital required before the property becomes income-producing.

Vacancy During Renovation

Where refurbishment is required, the calculator also captures the expected renovation period.

This helps highlight that time spent preparing a property can delay income generation.

Operating Costs

The model includes recurring HMO operating costs such as:

Buildings insurance

Council tax

Cleaning

Gas and electricity

Water

Broadband

Maintenance

Other running costs

These costs are important because HMO gross income can look attractive, but net yield depends heavily on ongoing operating expenditure.

Property Management Fees

The calculator allows investors to model either self-management or a letting provider fee.

Professional HMO management can reduce operational workload but materially affects net income and net yield.

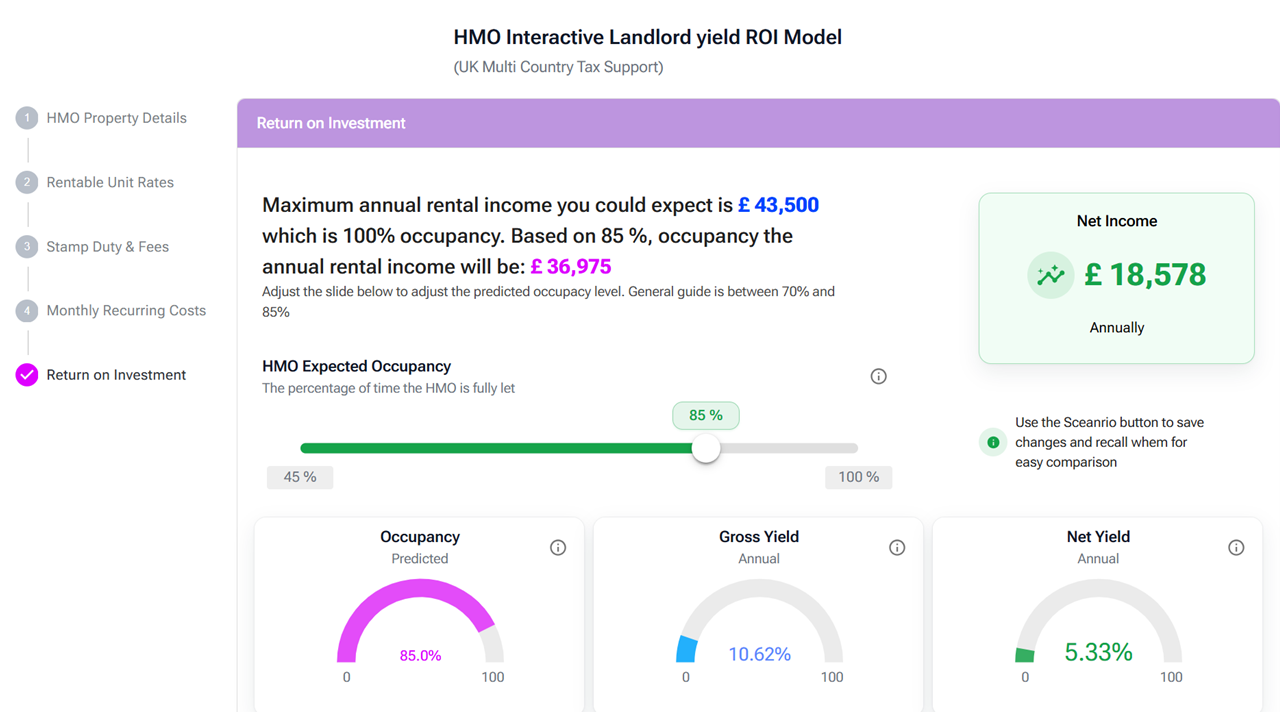

Occupancy Rate

The calculator adjusts projected income by expected occupancy.

This is critical because HMO returns are sensitive to void periods, tenant churn, seasonal demand, and local rental market strength.

Metrics Explained

Gross Income

Gross Income estimates the annual rental income before operating costs are deducted.

The calculator builds this from the monthly rent of each room or unit and adjusts it by the expected occupancy rate.

Monthly Gross Income

Monthly Gross Income shows the expected rental income in a typical month before recurring costs.

This helps investors understand the headline income potential of the property.

Monthly Costs

Monthly Costs estimate the recurring cost of operating the HMO.

This includes items such as management fees, ground rent, service charges, insurance, council tax, utilities, cleaning, broadband, and other running costs.

Net Monthly Income

Net Monthly Income estimates the remaining monthly income after recurring costs have been deducted from occupancy-adjusted rental income.

This is one of the most practical metrics for investors because it shows expected monthly cashflow before financing, tax, and personal circumstances.

Annual Net Income

Annual Net Income shows the projected yearly income after recurring operating costs.

This helps investors compare one HMO opportunity against another on a like-for-like annual basis.

Gross Yield

Gross Yield compares expected annual rental income with the total capital invested in the property and one-off purchase costs.

It provides a headline measure of rental return before recurring operating costs.

Net Yield

Net Yield compares annual income after recurring costs with the total capital invested.

This is usually the more useful yield metric because it accounts for the ongoing cost of operating the HMO.

Total Capital Outlay

Total Capital Outlay estimates the upfront investment required to purchase and prepare the property.

This includes the purchase price, regional property transaction tax, survey fees, legal fees, other one-off purchase costs, and refurbishment costs where applicable.

Property Transaction Tax

The calculator estimates the regional property transaction tax based on the selected purchase location.

This is important because England, Scotland, and Wales use different systems and rates, and additional property rules can materially increase upfront costs.

Why Net Yield Matters

Gross yield is useful for quickly comparing properties, but it can overstate the attractiveness of an HMO investment.

HMOs often involve higher operating costs than single-let properties. Investors may need to account for utilities, council tax, broadband, cleaning, maintenance, management fees, licensing requirements, and compliance costs.

Net yield gives a more realistic view of investment performance because it reflects the income left after recurring operating costs.

This calculator helps investors move beyond headline rental income and understand whether the property is likely to produce a sustainable return.

Who This Calculator Is For

HMO Property Investors

Estimate gross yield, net yield, income, and capital requirements before making an offer.

Buy-to-Let Landlords

Compare HMO returns against standard single-let investment opportunities.

Property Sourcers

Present more structured investment assumptions to prospective buyers.

Letting Agents and HMO Managers

Model income, management fees, operating costs, and occupancy assumptions.

Finance and Mortgage Brokers

Support conversations around rental income, affordability, and investment viability.

Property Consultants

Build clearer investor-facing business cases using property-specific assumptions.

Frequently Asked Questions

How is HMO rental yield calculated?

The calculator estimates annual rental income from the rentable rooms or units, adjusts this by occupancy, and compares it with the total capital invested.

What is the difference between gross yield and net yield?

Gross yield looks at rental income before operating costs. Net yield accounts for recurring costs such as management fees, utilities, insurance, service charges, council tax, cleaning, broadband, and maintenance.

Why does occupancy matter?

Occupancy affects how much rent is actually collected over the year. A property may have strong headline room rents, but void periods or tenant turnover can reduce realised income.

Does this calculator include stamp duty?

Yes. The model includes regional property purchase tax logic for England, Scotland, and Wales. These systems differ, so the selected region affects the estimated upfront cost.

Does an HMO need a licence?

A large HMO usually needs a licence where 5 or more people from more than one household share facilities. Smaller HMOs may also need licensing depending on local council rules.

Why are operating costs so important for HMOs?

HMOs often include costs that may not apply in the same way to single-let properties, such as inclusive utilities, broadband, cleaning, higher management complexity, and ongoing compliance-related costs.

Build a Stronger HMO Investment Case

Whether you are assessing a new HMO purchase, comparing investment opportunities, or modelling the impact of occupancy and running costs, this calculator helps estimate the true financial performance of a UK HMO investment.

Use the model to explore room-level rents, regional purchase costs, operating expenses, net income, and yield before committing capital.